Wendy's Wednesday.

Listen, I know this is even after a 20% move up. I’ll be honest, I do not fully understand the leverage situation at WEN. However, an easy step in the right direction would be to cancel the dividend and put that money towards paying off the debt. However, they need U.S. sales to stop falling. In Q1 2026, U.S. same-restaurant sales were down 7.8%. Margins also tell us that the business is consistently operationally stable and that outside factors are what are eating into Wendy’s profitability and ability to sustain its debt.

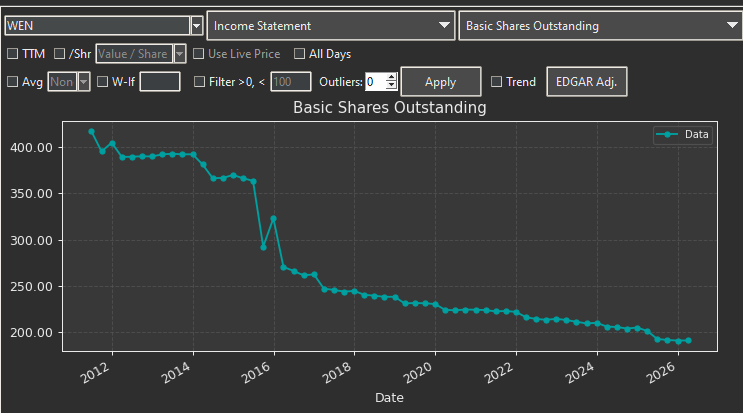

Management has already expressed some upcoming changes: new value platforms, premium burger upgrades, new chicken sandwiches, operational improvements, and international expansion including a China franchise agreement for up to 1,000 restaurants over 10 years. Management also said Q1 reflected the early stage of a turnaround. The fix is simple but slow: earn profits and retain them. Book equity will rise if retained earnings grow faster than dividends/buybacks reduce it.

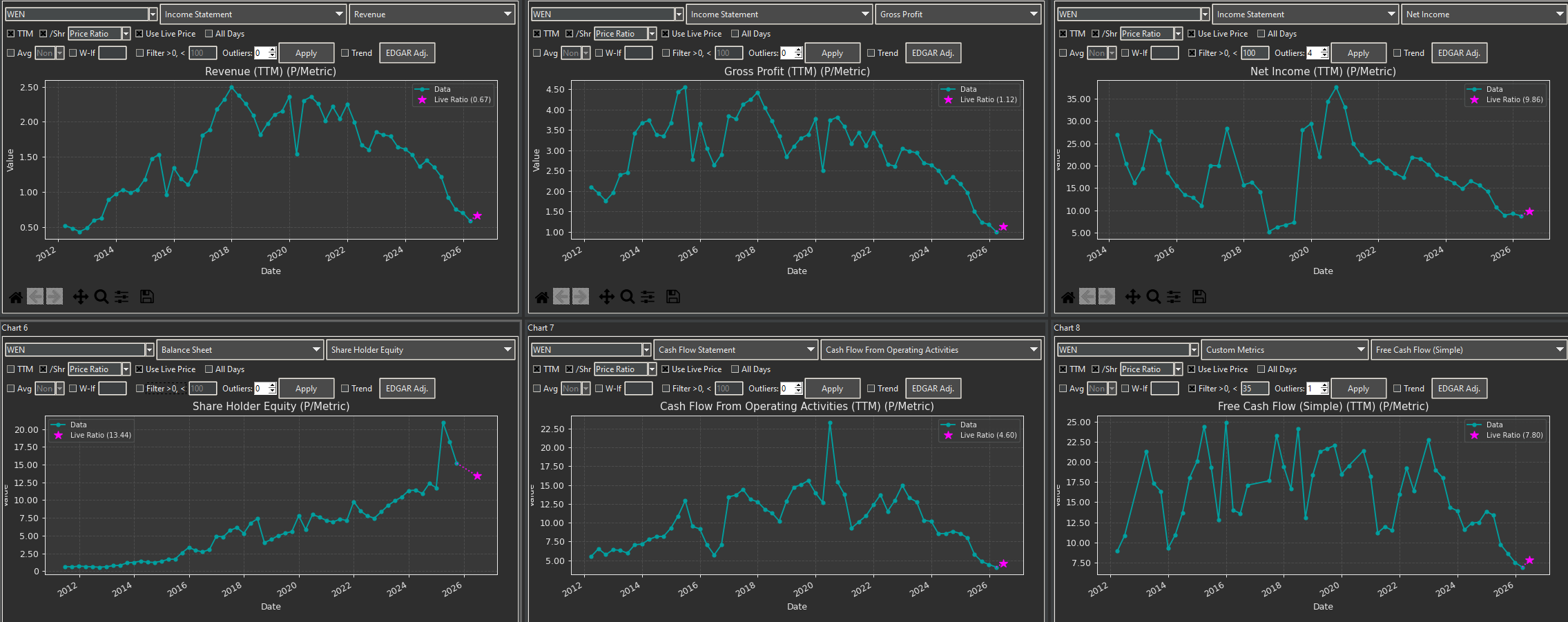

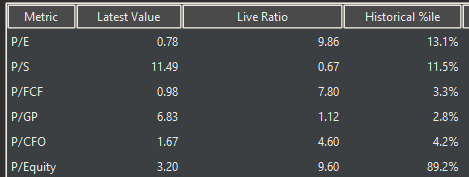

No buybacks, maybe a dividend cut, pay down debt, close weak restaurants, fix traffic, then maybe later resume capital returns. Right now, every dollar sent to shareholders is a dollar not used to reduce the thing making the stock risky. So have they? In early 2025, they changed the dividend policy to a target payout of 50%–60% of adjusted earnings, moving the quarterly dividend from $0.25 to $0.14. Their “Project Fresh” turnaround includes brand revitalization, operational excellence, system optimization, and capital allocation. In Q1 2026 they talked about the Biggie platform, upgraded burgers, new chicken sandwiches, and better order accuracy/customer satisfaction. The stock is already around 8.2x–8.5x EV/EBITDA. So, on EBITDA, it is almost near bottom prices. Would I have liked it before the move up? Who would not want near 7x multiples.

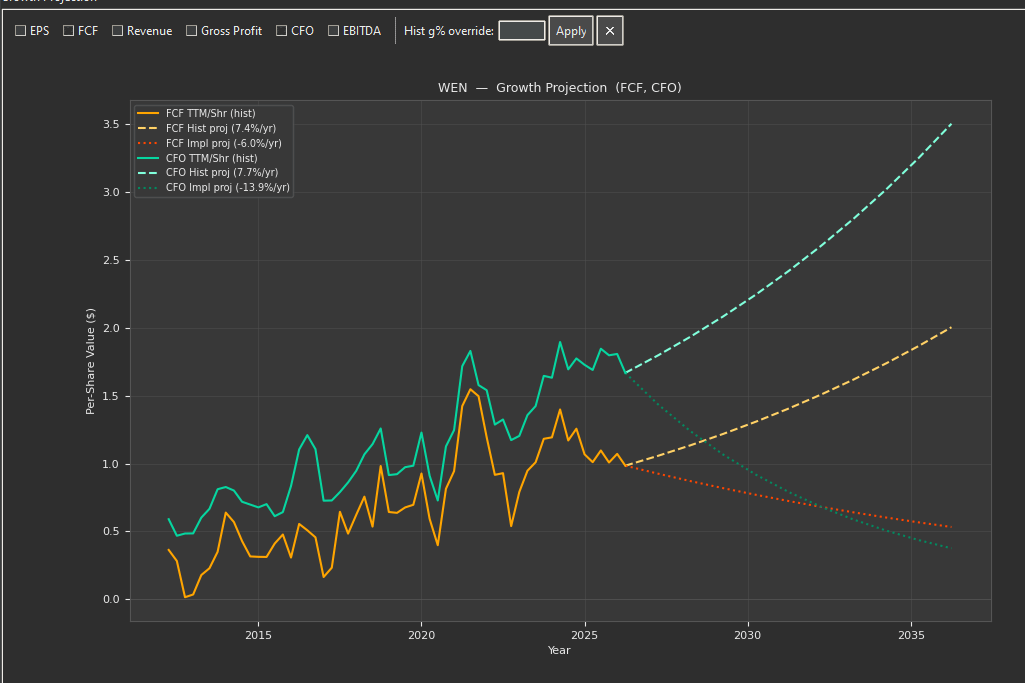

Even the market seems to think they are going to guide down their cash flows aggressively. I do not think this wide of a change will happen.

It’s truly low enough that there is that margin of safety.

That’s all.